Double materiality is a concept that is gaining increasing importance in the world of sustainability and corporate responsibility. It represents the union of two distinct sets of considerations: impact materiality and financial materiality. Double materiality refers to the concept that both financial and non-financial factors, such as environmental, social, and governance (ESG) considerations, are significant and interconnected in assessing a company's risks and opportunities.

This notion departs from traditional approaches that often see these two aspects as overlapping or only take into account financial materiality (such as ISSB). Instead, it acknowledges that a sustainability or Environmental, Social, and Governance (ESG) matter can have double materiality if it is material from either an impact or perspective, a financial perspective, or both.

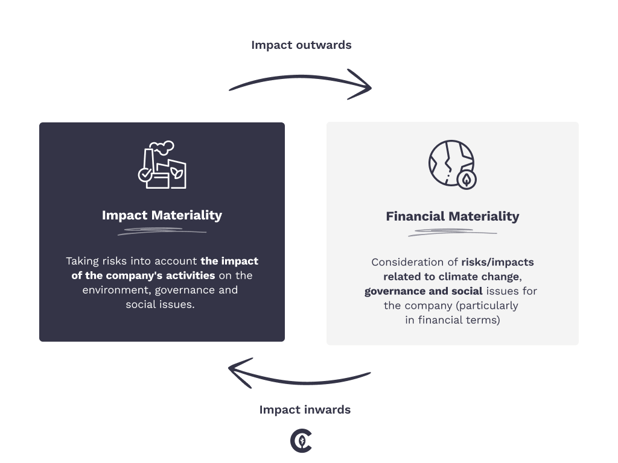

What is the difference between impact materiality and financial materiality?

Impact materiality focuses on the effects a company's operations and policies have on the environment and society. This could include factors like carbon emissions, labor practices, or community engagement. Financial materiality, on the other hand, deals with how these factors affect the company's financial performance and value. It includes the assessment of ESG-related risks and opportunities that may influence the company's profitability, financing capacity, reputation, regulatory compliance and long-term viability.

The concept of double materiality emphasizes that these two components are not always overlapping; a matter can be material from one perspective but not the other, or it can be material from both. This broader view encourages companies to consider a wider range of factors in their decision-making and reporting.

For instance, in the consumer goods industry, a company might choose to implement sustainable sourcing practices for the raw materials used in their products. This decision could be driven by an impact materiality perspective, recognizing the importance of preserving natural resources and supporting ethical labor practices. At the same time, it might also be considered from a financial materiality standpoint, as sustainable sourcing can reduce risks in the supply chain, potential scarcity of raw materials, enhance brand reputation, and potentially lead to cost savings or higher sales.

The concept of double materiality is significant because it pushes companies to go beyond traditional financial reporting and consider the broader impact of their operations which will be also strengthened by the CS3D (Corporate Sustainability Due Diligence Directive) in the coming years that will foster sustainability and responsible corporate behavior and to anchor human rights and environmental considerations in companies’ operations and corporate governance (due diligence/ duty of care). This holistic approach is increasingly demanded by investors, regulators, and consumers who are concerned not just with financial returns, but also with environmental and social impacts.

How is double materiality related to CSRD?

Since the start of its application in January 2024, the Corporate Sustainability Reporting Directive ("CSRD") represents a significant expansion of the scope of mandatory extra-financial reporting by companies within the EU.

The CSRD will replace the previous Non-Financial Reporting Directive ("NFRD") and aims to:

- Extend the number of companies subject to non-financial reporting.

- Extend the range of non-financial information for which reporting is mandatory.

- Standardize reporting practices.

Double materiality is integrated with the reporting aspect of CSRD, as it’s a compulsory exercise in itself and an exercise that determines the reporting obligations of the companies concerned. This is the first exercise that concerned companies need to perform. ESRS 2 - General Information makes it universally mandatory to disclose material impacts, risks, and opportunities to a company's strategy and business model. It also makes it mandatory to describe the process by which companies identify and prioritize their Impacts, Risks, and Opportunities (IROs) indicators.

As we have already seen, the CSRD is made up of universally mandatory standards, and standards becoming mandatory based on the positive materiality assessment of the company concerned. For example, to give you an idea, a company with a material impact on water, or whose business model relies on water resources, is required to publish information relating to ESRS 2 - General Information.

Share this

CSRD 2025 Definition: Understanding Non-Financial Reporting for EU Companies

The Booming of Net-Zero Commitments